COVID-19 Payroll Tax Relief Raises Questions

As part of COVID-19 relief President Trump issued a memorandum on Aug. 8, 2020, and the Department of Treasury and the Internal Revenue Service issued Notice 2020-65 on Aug. 28, 2020, which permits the deferral of the withholding, deposit and payment of the employee portion of Social Security taxes for certain wages.

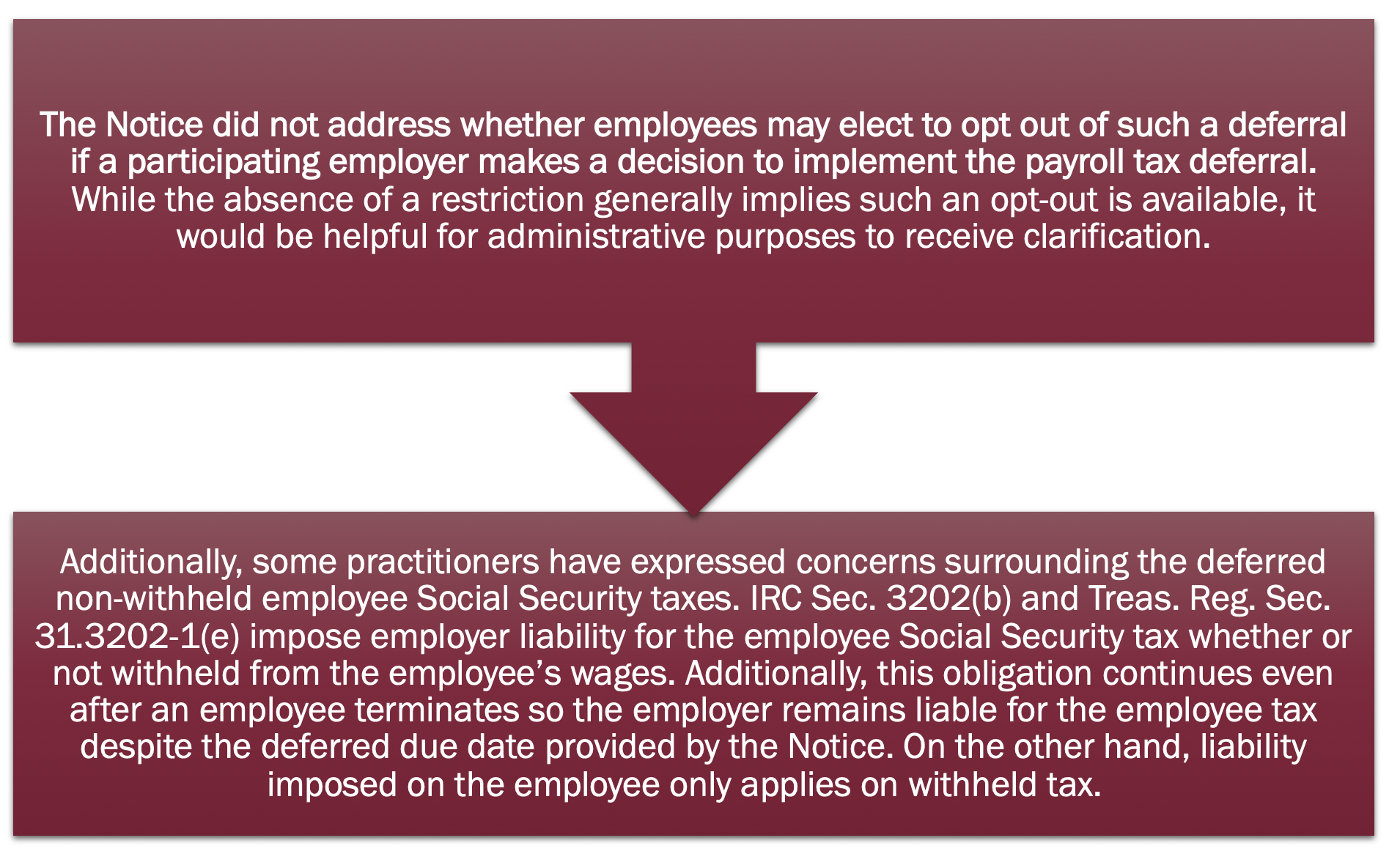

The payroll tax deferral period is voluntary not required.

This means a participating employer has the option to defer its payroll tax for eligible individuals from Sept. 1, 2020 through Dec. 31, 2020, but would then be required to double subsequent payroll tax withholding for such individuals from Jan. 1, 2021 through April 30, 2021. If arrangements are not made to collect the deferred taxes, interest and penalties will begin to accrue May 1, 2021. “Eligible individuals” would be employees whose pay is less than $4,000 in a biweekly period, including salaried workers earning less than $104,000 per year. (Note: eligibility of employees must be tested every pay period by the employer.)

This relief has raised questions and concerns –

From a client fund perspective, if Zenith American Solutions is acting as agent, a participating employer will need to provide notice to the client fund and Zenith American Solutions, its directed TPA, of its decision to defer payroll taxes in regards to disability benefits and would need to confirm each week the list of eligible employees/participants who are subject to the payroll tax deferral. To the extent Zenith American Solutions prepares Form 1099s for a client fund as part of our services, such deferral of withholding would not be reflected in 2020 but would be accounted for in 2021 when subsequent withholding occurs.

Given that employers remain liable for the 2020 non-withheld taxes it is unlikely many employers will implement the payroll tax deferral unless additional relief is provided. Employers who choose to implement the deferral should consult with their legal advisors and payroll tax vendors regarding the additional action needed. Additionally, as noted above, the employer should immediately notify the client fund and Zenith to the extent coordination of any necessary action by the client fund is required to address the participating employer’s deferral and subsequent payment of payroll taxes.